Nitesh Jain, Director, CRISIL Ratings Limited

Nitesh Jain, Director, CRISIL Ratings Limited

A massive spurt in data consumption and tariffs alike has helped telecom operators in India recover gradually over the course of the Covid-19 pandemic, after bleeding through fiscals 2017-2019 due to tariff wars and the pending verdict on the matter of adjusted gross revenue.

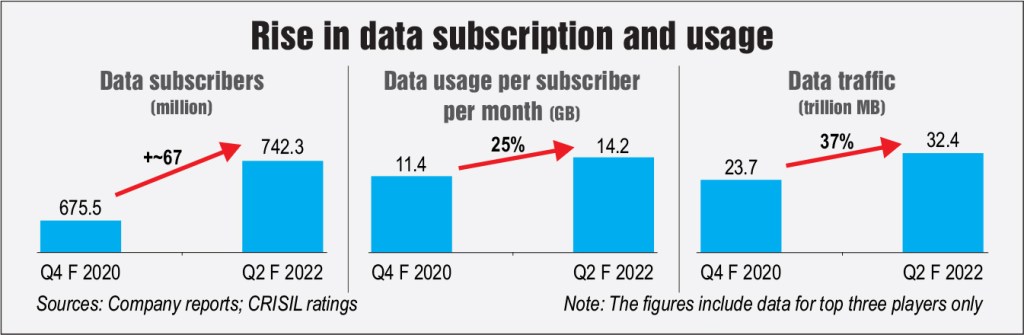

The shift to work from home and online studies has whetted the data needs of people. Between March 2020 and September 2021, the top three telcos added around 67 million data subscribers and saw the average data usage per subscriber increase by around 25 per cent to over 14 GB per month, leading to data traffic soaring by around 37 per cent.

Added to the increased consumption, operators benefitted from tariff hikes of up to 50 per cent made in December 2019, just before the pandemic took hold. The heightened need for data has also compelled subscribers to upgrade their tariff plans.

All of this has translated into a higher average revenue per use of around Rs 147 for the quarter ended September 2021, compared to around Rs 137 for the quarter ended March 2020. Tariff hikes, subscriber additions, and customer up-trading have together pushed up the sector topline to around 10 per cent and earnings before interest, taxes, depreciation and amortisation (EBITDA) by around 30 per cent.

Thereafter, telcos have selectively revised the pricing of their lower-tariff entry level plans, because between March 2020 and September 2021, telcos added around 51 million rural internet subscribers compared to around 41 million from urban India. Besides, the launch of entry-level smartphones with easy financing schemes meant a further push to rural subscriber addition.

Thereafter, telcos have selectively revised the pricing of their lower-tariff entry level plans, because between March 2020 and September 2021, telcos added around 51 million rural internet subscribers compared to around 41 million from urban India. Besides, the launch of entry-level smartphones with easy financing schemes meant a further push to rural subscriber addition.

Telcos have also hiked prices of post-paid plans, bolstering their toplines as post-paid subscribers account for over 25 per cent of their revenue base despite being only around 5 per cent of the overall subscriber base.

Moreover, cognisant of the sector’s criticality, the government approved a number of structural and process reforms in September 2021, providing immediate cash-flow relief and helping telcos lower their statutory and interest costs through prepayment of past spectrum dues.

That said, a material increase in cash-flows is imperative before the players roll out 5G mobile services and dial up returns. The trend of higher data consumption and higher tariffs augurs well, to this end.

The top three players raised prepaid tariffs by over 20 per cent in November. Until then, though they were revising tariffs selectively, the telcos had held back on another round of broad-based tariff hikes in the prepaid segment. This move, together with robust demand for data, should give a further fillip to the revenue and profitability of telcos next fiscal, with EBITDA estimated to grow by around 40 per cent during fiscals 2021-2023 to around Rs 1 trillion.

The top three players raised prepaid tariffs by over 20 per cent in November. Until then, though they were revising tariffs selectively, the telcos had held back on another round of broad-based tariff hikes in the prepaid segment. This move, together with robust demand for data, should give a further fillip to the revenue and profitability of telcos next fiscal, with EBITDA estimated to grow by around 40 per cent during fiscals 2021-2023 to around Rs 1 trillion.

Cash-flow relief measures provided by the government will, along with the expected EBITDA growth, support investment in 5G mobile service networks over the medium term.

There is a catch, though. An increase in data consumption will require these players to continue to invest in building infrastructure. Telcos will likely adopt a calibrated approach initially and buy 5G spectrum only in metros and Category A circles, where data consumption is higher compared to other circles, though it would be a function of the final reserve prices.

There is a catch, though. An increase in data consumption will require these players to continue to invest in building infrastructure. Telcos will likely adopt a calibrated approach initially and buy 5G spectrum only in metros and Category A circles, where data consumption is higher compared to other circles, though it would be a function of the final reserve prices.